Introduction

Managing education debt can feel overwhelming, but understanding the right Student loan repayment options can completely change your financial future. Whether you recently graduated, are still in school, or have been paying loans for years, choosing the correct repayment strategy can save you thousands of dollars and reduce financial stress.

In this detailed guide, we will explore all major Student loan repayment options, including federal plans, private loan strategies, forgiveness programs, refinancing, consolidation, and smart payoff techniques. This SEO-optimized, beginner-friendly guide will help you make informed decisions and confidently manage your education debt.

What Are Student Loan Repayment Options?

Student loan repayment options are structured plans and strategies that allow borrowers to repay their student loans based on their financial situation. These options determine:

- Monthly payment amount

- Loan repayment duration

- Interest accumulation

- Eligibility for forgiveness

- Total cost of the loan

Choosing the right repayment plan depends on income, career path, financial goals, loan type, and family size.

Types of Student Loans

Before choosing among different Student loan repayment options, you must understand the type of loan you have.

1. Federal Student Loans

Federal student loans are funded by the U.S. government and are designed to make higher education more affordable for students and families. These loans typically offer lower interest rates, flexible repayment structures, borrower protections, and access to various Student loan repayment options, including income-driven plans and forgiveness programs.

Below is a detailed explanation of the most common types of federal student loans:

✅ Direct Subsidized Loans

What Are Direct Subsidized Loans?

Direct Subsidized Loans are federal loans available to undergraduate students who demonstrate financial need. These loans are called “subsidized” because the U.S. Department of Education pays the interest under certain conditions.

Who Is Eligible?

- Undergraduate students only

- Must demonstrate financial need through the FAFSA (Free Application for Federal Student Aid)

- Must be enrolled at least half-time

Key Benefits

- Government Pays Interest During School

- While you are enrolled at least half-time

- During the 6-month grace period after graduation

- During approved deferment periods

- Lower overall interest cost compared to unsubsidized loans

- Access to flexible Student loan repayment options

Loan Limits

Loan limits depend on:

- Year in school

- Dependency status

- School cost

There are annual and lifetime borrowing limits.

Repayment Flexibility

Direct Subsidized Loans qualify for:

- Standard Repayment

- Graduated Repayment

- Extended Repayment

- Income-Driven Repayment (IDR) plans

- Public Service Loan Forgiveness (PSLF)

Because of the interest subsidy and flexible Student loan repayment options, these loans are often considered the most favorable type of federal loan.

✅ Direct Unsubsidized Loans

What Are Direct Unsubsidized Loans?

Direct Unsubsidized Loans are federal loans available to undergraduate, graduate, and professional students. Unlike subsidized loans, these do not require financial need.

Who Is Eligible?

- Undergraduate students

- Graduate students

- Professional students

- No financial need requirement

Key Features

- Interest Accrues Immediately

- Interest starts accumulating as soon as the loan is disbursed

- You are responsible for all interest

- Flexible use of funds for tuition, housing, books, and other education-related expenses

- Higher borrowing limits for graduate students

Interest Capitalization

If unpaid interest accumulates during school or deferment, it may be added to the principal balance. This increases the total repayment amount.

Repayment Options

Just like subsidized loans, Direct Unsubsidized Loans qualify for all federal Student loan repayment options, including:

- Income-Driven Repayment plans

- Loan forgiveness programs

- Consolidation

Although they accrue interest immediately, they still offer strong borrower protections and flexibility.

✅ Direct PLUS Loans

What Are Direct PLUS Loans?

Direct PLUS Loans are federal loans available to:

- Graduate or professional students (Grad PLUS Loans)

- Parents of dependent undergraduate students (Parent PLUS Loans)

These loans help cover education costs not already covered by other financial aid.

Credit Requirement

Unlike other federal loans, PLUS Loans require:

- A credit check

- No adverse credit history

However, credit standards are generally more flexible than private loans.

Key Features

- Can cover up to the full cost of attendance (minus other aid)

- Higher interest rates compared to subsidized and unsubsidized loans

- Origination fees apply

Repayment Terms

- Repayment usually begins immediately after disbursement

- Parents can request deferment while the student is in school

- Graduate students qualify for a grace period

Repayment Flexibility

Direct PLUS Loans are eligible for several Student loan repayment options, including:

- Standard Repayment

- Graduated Repayment

- Extended Repayment

- Income-Contingent Repayment (after consolidation for Parent PLUS Loans)

Parent PLUS Loans must be consolidated into a Direct Consolidation Loan to access income-driven repayment.

Despite higher interest rates, PLUS Loans still offer more flexible Student loan repayment options than private loans.

✅ Direct Consolidation Loans

What Is a Direct Consolidation Loan?

A Direct Consolidation Loan allows borrowers to combine multiple federal student loans into one single loan with one monthly payment.

How It Works

- Your existing federal loans are paid off

- A new consolidated loan is issued

- The new interest rate is a weighted average of existing rates (rounded up slightly)

Benefits

- Simplifies repayment (one payment instead of multiple)

- Provides access to additional Student loan repayment options

- Can make loans eligible for Public Service Loan Forgiveness

Important Considerations

- Consolidation may extend repayment period

- Total interest paid may increase

- Forgiveness progress may reset in some cases

When Is Consolidation Helpful?

- If you have multiple loan servicers

- If you want to switch to an income-driven plan

- If you want to qualify for forgiveness programs

Direct Consolidation Loans play an important role in expanding federal Student loan repayment options.

Why Federal Student Loans Offer the Most Flexible Student Loan Repayment Options

Federal loans provide several advantages:

1. Income-Driven Repayment Plans

Payments based on income and family size.

2. Forgiveness Programs

Including:

- Public Service Loan Forgiveness

- Teacher Loan Forgiveness

- IDR forgiveness after 20–25 years

3. Deferment and Forbearance

Temporary payment relief during hardship.

4. Fixed Interest Rates

Predictable payments.

5. No Prepayment Penalties

You can pay extra anytime.

These features make federal loans far more flexible compared to private loans when evaluating Student loan repayment options.

2. Private Student Loans

These are offered by banks, credit unions, and private lenders. They usually:

- Have fixed or variable interest rates

- Offer fewer flexible repayment options

- Do not qualify for federal forgiveness programs

Understanding your loan type helps you choose the best Student loan repayment options.

When Does Repayment Start?

Most federal student loans offer:

- A 6-month grace period after graduation

- Deferment while enrolled at least half-time

Private lenders may have different rules.

Understanding when repayment starts helps you plan your Student loan repayment options effectively.

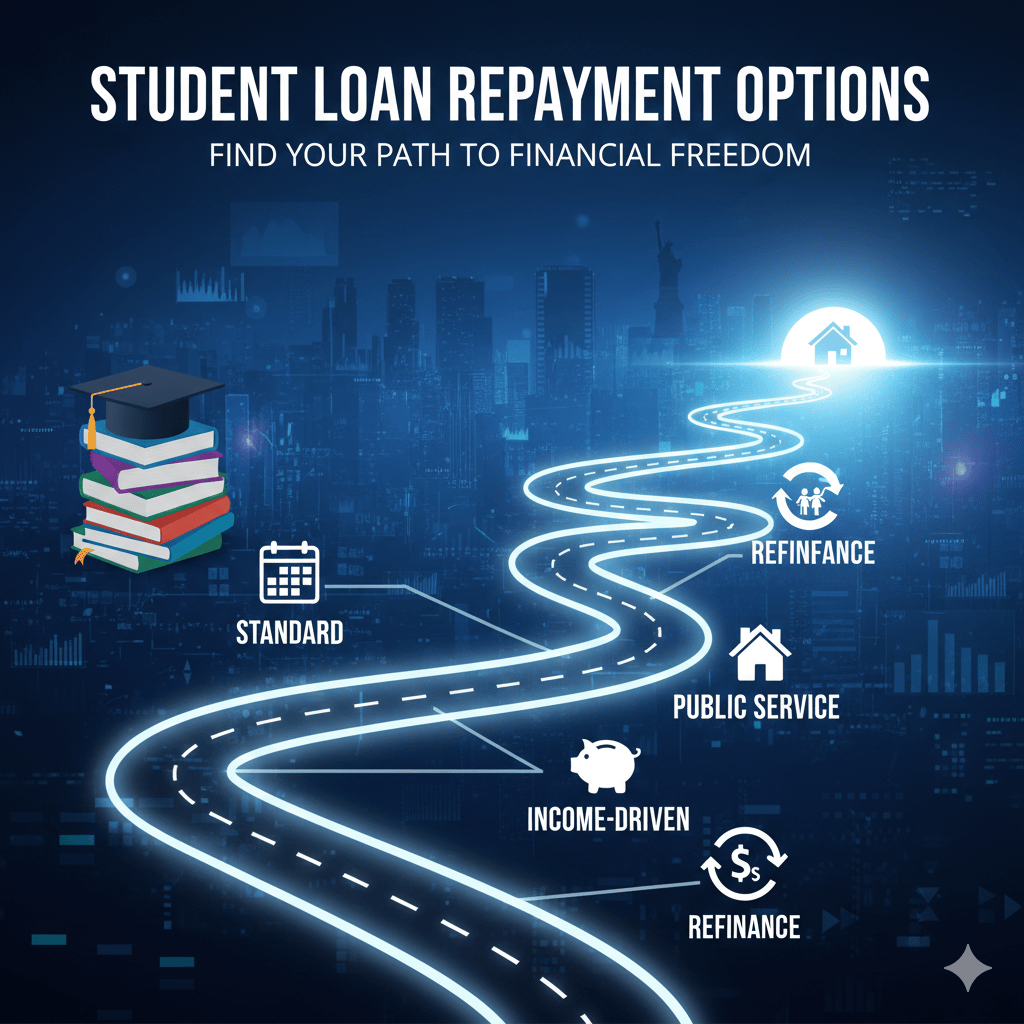

Federal Student Loan Repayment Options

Federal loans offer multiple structured Student loan repayment options. Let’s explore them in detail.

1. Standard Repayment Plan

Overview

- Fixed monthly payments

- 10-year repayment term

Benefits

- Pay less interest overall

- Fastest payoff among all plans

- Predictable monthly payments

Best For

- Borrowers with stable income

- Those who want to become debt-free quickly

This is one of the simplest Student loan repayment options.

2. Graduated Repayment Plan

Overview

- Payments start low

- Increase every two years

- 10-year term

Benefits

- Easier start for entry-level salaries

Drawbacks

- Higher total interest

Graduated plans are helpful Student loan repayment options if you expect salary growth.

3. Extended Repayment Plan

Overview

- Repayment up to 25 years

- Fixed or graduated payments

Benefits

- Lower monthly payments

Drawbacks

- More interest paid over time

This is one of the flexible Student loan repayment options for borrowers with larger loan balances.

Income-Driven Repayment (IDR) Plans

Income-driven plans are among the most powerful Student loan repayment options available.

These plans calculate payments based on income and family size.

1. Income-Based Repayment (IBR)

- 10–15% of discretionary income

- 20–25 year forgiveness

Great for borrowers with high debt relative to income.

2. Pay As You Earn (PAYE)

- 10% of discretionary income

- 20-year forgiveness

An excellent choice among modern Student loan repayment options.

3. Revised Pay As You Earn (REPAYE) / SAVE Plan

- Based on income percentage

- Interest subsidies available

- Forgiveness after 20–25 years

This plan is highly popular among income-driven Student loan repayment options.

4. Income-Contingent Repayment (ICR)

- 20% of discretionary income

- 25-year forgiveness

One of the older Student loan repayment options, but still useful for certain borrowers.

Public Service Loan Forgiveness (PSLF)

Public Service Loan Forgiveness is a powerful benefit tied to certain Student loan repayment options.

Eligibility

- Work for government or nonprofit

- Make 120 qualifying payments

- Be on an income-driven plan

After 10 years of payments, remaining balance is forgiven tax-free.

Teacher Loan Forgiveness

Teachers working in low-income schools may qualify for forgiveness up to $17,500.

This forgiveness works best when paired with specific Student loan repayment options.

Student Loan Consolidation

Direct Consolidation Loans combine multiple federal loans into one.

Benefits

- One payment

- Access to income-driven plans

Drawbacks

- May reset forgiveness progress

Consolidation is one of the structural Student loan repayment options that simplifies payments.

Student Loan Refinancing

Refinancing replaces existing loans with a new private loan at a lower interest rate.

Benefits

- Lower interest rate

- Reduced monthly payment

- Shorter repayment term

Risks

- Lose federal benefits

- No access to federal forgiveness

Refinancing is a strategic choice among private Student loan repayment options.

Choosing the Best Student Loan Repayment Options

When selecting among different Student loan repayment options, consider:

- Income level

- Career path

- Job stability

- Total loan balance

- Financial goals

Strategies to Pay Off Student Loans Faster

Even with the best Student loan repayment options, smart strategies can accelerate repayment.

1. Make Extra Payments

Apply extra funds toward principal.

2. Biweekly Payments

Split payments to reduce interest.

3. Use Windfalls

Tax refunds, bonuses, or gifts.

4. Employer Assistance Programs

Some companies offer repayment assistance.

Avoiding Common Mistakes

When evaluating Student loan repayment options, avoid:

- Ignoring income-driven eligibility

- Refinancing federal loans without research

- Missing recertification deadlines

- Defaulting due to lack of planning

What Happens If You Can’t Pay?

Federal loans offer protections:

- Deferment

- Forbearance

- Income-driven adjustments

These safety nets are important parts of federal Student loan repayment options.

Tax Implications

Some forgiven balances may be taxable (except PSLF).

Always consider tax effects when reviewing Student loan repayment options.

Comparing Federal vs Private Student Loan Repayment Options

| Feature | Federal Loans | Private Loans |

|---|---|---|

| Income-Driven Plans | Yes | Rare |

| Forgiveness Programs | Yes | No |

| Flexible Deferment | Yes | Limited |

| Refinancing | Yes | Yes |

Federal Student loan repayment options offer more protections.

Sample Repayment Scenario

Loan: $40,000

Interest Rate: 6%

- Standard Plan: $444/month, 10 years

- IDR Plan: $250/month initially

- Extended Plan: $300/month, 25 years

Comparing these Student loan repayment options helps borrowers make informed decisions.

Should You Pay Off Student Loans Early?

Pros:

- Save interest

- Financial freedom

- Better credit score

Cons:

- May ignore investing

- Reduced liquidity

Balance your goals when choosing Student loan repayment options.

How to Apply for Income-Driven Plans

- Visit StudentAid.gov

- Submit income documentation

- Choose preferred plan

- Recertify annually

Applying correctly ensures smooth access to federal Student loan repayment options.

10 High-Ranking FAQs

1. What are the best student loan repayment options available in 2026?

The best Student loan repayment options depend on your income, loan type, and financial goals. Federal borrowers can choose from Standard, Graduated, Extended, and Income-Driven Repayment (IDR) plans. If you work in public service, Public Service Loan Forgiveness (PSLF) may be ideal. Private loan borrowers may consider refinancing for lower interest rates.

2. How do income-driven student loan repayment options work?

Income-driven Student loan repayment options calculate your monthly payment based on your income and family size instead of your total loan balance. Most IDR plans require 10–20% of discretionary income and offer forgiveness after 20–25 years of qualifying payments.

3. Can I change my student loan repayment option later?

Yes, federal borrowers can switch between different Student loan repayment options at any time. However, changing plans may affect your total interest paid or reset progress toward forgiveness in certain cases. Always review the impact before switching.

4. What happens if I miss a student loan payment?

If you miss payments under your chosen Student loan repayment options, your loan may become delinquent and eventually go into default. This can damage your credit score and lead to wage garnishment. If you’re struggling, apply for deferment, forbearance, or an income-driven plan immediately.

5. Are student loan repayment options different for federal and private loans?

Yes. Federal loans offer flexible Student loan repayment options, including income-driven plans and forgiveness programs. Private lenders usually offer limited repayment flexibility and do not provide federal forgiveness benefits.

6. What is the fastest way to repay student loans?

The fastest way to eliminate debt under most Student loan repayment options is the Standard Repayment Plan (10 years) combined with extra principal payments. Making biweekly payments and applying bonuses or tax refunds toward the loan can also accelerate repayment.

7. Do student loan repayment options affect my credit score?

Yes. Making on-time payments under any Student loan repayment options improves your credit score. However, missed payments or default can significantly lower your credit rating and stay on your report for years.

8. Is student loan forgiveness real?

Yes, forgiveness is available under specific Student loan repayment options, such as Public Service Loan Forgiveness (PSLF) and income-driven plans. However, strict eligibility requirements must be met, and you must make qualifying payments for a certain number of years.

9. Should I refinance my student loans?

Refinancing can lower interest rates and monthly payments, making it one of the strategic private Student loan repayment options. However, refinancing federal loans removes access to income-driven plans and forgiveness programs, so consider carefully before deciding.

10. Which student loan repayment option lowers monthly payments the most?

Income-driven Student loan repayment options typically offer the lowest monthly payments because they are based on your income rather than your loan balance. Extended repayment plans can also reduce monthly payments but may increase total interest costs.

✅ Final Thought

Student loan debt can feel heavy, but it does not have to control your financial future. The most important step is understanding your Student loan repayment options and choosing a plan that fits your current reality — not someone else’s situation. There is no “one-size-fits-all” solution. What works for a high-income professional may not work for someone just starting their career.

The smartest borrowers review their Student loan repayment options regularly, especially when income changes, career paths shift, or life circumstances evolve. Flexibility is one of the biggest advantages of federal repayment plans, and using that flexibility wisely can save thousands of dollars over time.

Remember, repayment is not just about lowering monthly payments — it’s about balancing debt with building savings, investing for retirement, and maintaining financial security. The right Student loan repayment options should support your long-term goals, not delay them.

Stay proactive, make payments on time, avoid default, and don’t hesitate to adjust your plan when necessary. With the right strategy, discipline, and knowledge, you can turn education debt into a manageable step toward financial independence.

Your degree is an investment in yourself — and with the right Student loan repayment options, you can protect that investment while building a strong and confident financial future.

✅ Conclusion: Choosing the Right Student Loan Repayment Options for Long-Term Financial Freedom

Navigating education debt can feel stressful and confusing, but the good news is that there are multiple Student loan repayment options designed to fit different financial situations. The key to success is not just making payments — it’s choosing a repayment strategy that aligns with your income, career goals, lifestyle, and long-term financial plans.

Throughout this guide, we explored federal and private Student loan repayment options, including Standard, Graduated, Extended, and Income-Driven Repayment (IDR) plans. Each option serves a different purpose. If you have a stable income and want to eliminate debt quickly, the Standard plan may help you pay less interest overall. If your income is limited or unpredictable, income-driven Student loan repayment options can provide flexibility and breathing room while keeping your loans in good standing.

One of the most powerful advantages of federal Student loan repayment options is access to forgiveness programs. Public Service Loan Forgiveness (PSLF), teacher loan forgiveness, and long-term IDR forgiveness can significantly reduce your repayment burden if you meet eligibility requirements. However, these programs require careful documentation, consistent payments, and patience. Understanding the rules is essential to maximize benefits.

For borrowers with private loans, refinancing may offer better interest rates and simplified payments. However, refinancing federal loans removes access to federal protections and forgiveness-based Student loan repayment options. Therefore, borrowers should evaluate both short-term savings and long-term risks before making this decision.

Another important takeaway is that repayment plans are not permanent. Many borrowers don’t realize they can switch between federal Student loan repayment options as their financial situation changes. Whether your income increases, decreases, or your career path shifts, reviewing your repayment plan annually can help you stay on track and avoid unnecessary interest costs.

In addition to selecting the right plan, smart repayment strategies can make a big difference. Making extra principal payments, setting up autopay, applying windfalls toward your loan, and avoiding missed payments can reduce your overall repayment timeline. Even small additional payments can save thousands in interest over time.

It’s also important to remember that student loan management is part of a bigger financial picture. While aggressively paying off debt can be beneficial, you should also balance emergency savings, retirement investing, and other financial priorities. The best Student loan repayment options are those that support both debt reduction and overall financial stability.

If you are struggling to make payments, do not ignore the problem. Federal Student loan repayment options include deferment, forbearance, and income-driven adjustments that can prevent default and protect your credit score. Taking early action is always better than waiting until the situation worsens.

Ultimately, education is an investment in your future. With the right Student loan repayment options, that investment does not have to become a lifelong burden. By understanding your choices, comparing plans carefully, and staying proactive, you can repay your loans confidently and move toward financial independence.

Take time to evaluate your income, career plans, and financial goals. Review your loans regularly. Ask questions. Stay informed. The right Student loan repayment options can transform debt from a source of stress into a manageable financial responsibility — and put you on the path toward long-term wealth and stability.