Introduction

Personal loans have become one of the most popular financial tools in India due to their flexibility, quick approval, and zero collateral requirement. However, one of the most important factors that borrowers must understand before applying is personal loan interest rates.

The personal loan interest rates you receive can significantly impact your EMI, total repayment amount, and overall financial burden. Even a small difference of 1–2% can lead to thousands of rupees in additional interest over time.

In this detailed guide, we will explain everything about personal loan interest rates, including current rates in India, factors affecting rates, calculation methods, comparison strategies, and tips to get the lowest rate.

What Are Personal Loan Interest Rates?

Personal loan interest rates refer to the cost charged by banks or lenders for borrowing money. It is usually expressed as a percentage per annum (p.a.).

When you take a personal loan, the lender charges interest on the principal amount, which you repay through EMIs (Equated Monthly Installments).

👉 For example:

If you borrow ₹1,00,000 at 12% personal loan interest rates, you will pay interest along with the principal amount over the loan tenure.

According to recent data, personal loan interest rates in India start from around 8.75% to 10% and can go up to 24% or more, depending on your profile.

Current Personal Loan Interest Rates in India (2026)

Understanding current personal loan interest rates helps you choose the best lender.

Average Interest Rate Range

- Public sector banks: 10% – 14%

- Private banks: 11% – 18%

- NBFCs: 13% – 24%

- Fintech lenders: 18% – 28%

Top Banks Offering Personal Loan Interest Rates

| Bank Name | Interest Rate |

|---|---|

| SBI | 10% – 15% |

| HDFC Bank | 9.99% – 24% |

| ICICI Bank | 9.99% – 16.5% |

| Axis Bank | 9.5% – 22% |

| Bank of Baroda | 10% onwards |

👉 This clearly shows that personal loan interest rates vary widely based on lender type and borrower profile.

Types of Personal Loan Interest Rates

Understanding different types of personal loan interest rates is crucial before applying.

1. Fixed Interest Rate

- Remains constant throughout the loan tenure

- EMI stays the same

- Best for stability

2. Floating Interest Rate

- Changes based on market conditions

- Linked to benchmarks like MCLR

- EMI may fluctuate

3. Reducing Balance Interest Rate

- Interest is calculated on the remaining principal

- More cost-effective

4. Flat Interest Rate

- Interest calculated on full loan amount

- Higher overall cost

👉 Most lenders in India use reducing balance personal loan interest rates.

How Personal Loan Interest Rates Work

To understand personal loan interest rates, you must know how lenders calculate them.

Key Concepts:

- Principal Amount

- Interest Rate

- Loan Tenure

- EMI

👉 Interest is calculated monthly on the outstanding balance, not the total amount.

According to experts, even a small change in personal loan interest rates directly impacts EMI and total repayment.

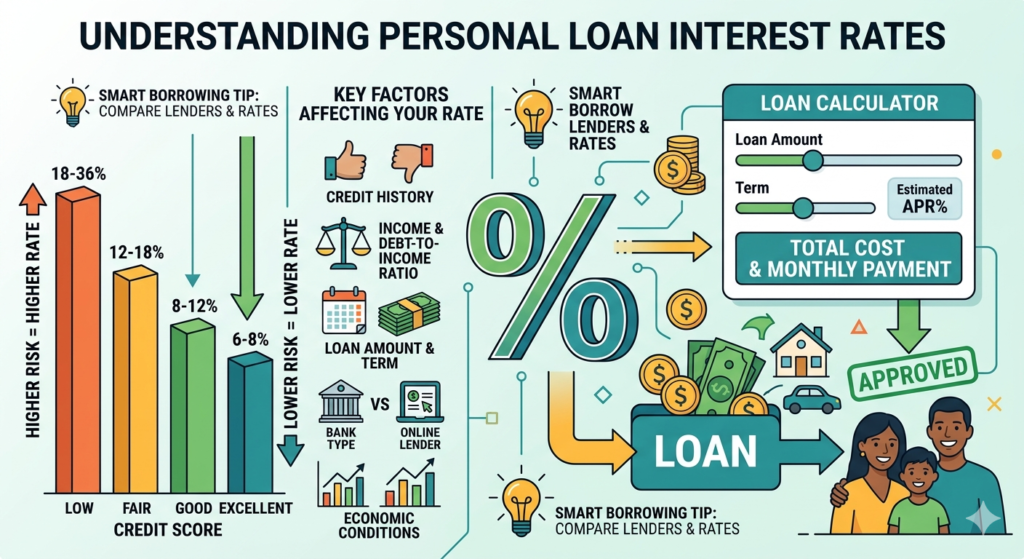

Factors Affecting Personal Loan Interest Rates

Several factors determine your personal loan interest rates:

1. Credit Score (CIBIL Score)

- 750+ → Lowest rates

- 650–750 → Moderate rates

- Below 650 → High rates

A higher credit score can help you secure personal loan interest rates as low as 9.99%.

2. Income Level

Higher income = lower risk = better personal loan interest rates

3. Employment Type

- Government employees → Lower rates

- Salaried professionals → Moderate rates

- Self-employed → Higher rates

4. Employer Reputation

Working in a reputed company improves chances of lower personal loan interest rates

5. Loan Amount

- Higher loan → lower rates (in some cases)

- Smaller loans → higher rates

6. Loan Tenure

- Longer tenure → higher total interest

- Short tenure → higher EMI but lower interest

7. Existing Liabilities

Higher EMIs reduce eligibility and increase personal loan interest rates

How to Calculate Personal Loan Interest Rates

To calculate EMI based on personal loan interest rates, use the formula:

EMI = [P × R × (1+R)^N] / [(1+R)^N – 1]

Where:

- P = Loan amount

- R = Monthly interest rate

- N = Tenure

👉 Most banks provide online EMI calculators for quick calculation.

Importance of Personal Loan Interest Rates

Understanding personal loan interest rates is important because:

- Determines EMI amount

- Affects total repayment

- Impacts affordability

- Helps compare lenders

Even a 1% increase in personal loan interest rates can increase your repayment significantly.

How to Get the Lowest Personal Loan Interest Rates

Here are proven strategies to get lower personal loan interest rates:

1. Maintain High Credit Score

Pay bills on time and avoid defaults.

2. Compare Multiple Lenders

Never choose the first offer.

3. Choose Short Tenure

Reduces total interest cost.

4. Maintain Stable Income

Steady job improves your profile.

5. Negotiate with Lenders

Banks may reduce personal loan interest rates for good customers.

6. Apply with Existing Bank

Existing customers often get better rates.

Public vs Private vs NBFC Interest Rates

Public Sector Banks

- Lowest personal loan interest rates

- Strict eligibility

Private Banks

- Faster approval

- Moderate personal loan interest rates

NBFCs

- Flexible approval

- Higher personal loan interest rates

Personal Loan Interest Rates vs Other Loans

| Loan Type | Interest Rate |

|---|---|

| Home Loan | 7% – 9% |

| Personal Loan | 10% – 24% |

| Loan Against Property | 8% – 12% |

👉 Personal loans have higher personal loan interest rates because they are unsecured.

Common Charges Along with Interest Rates

When considering personal loan interest rates, also check:

- Processing fee (1%–3%)

- Late payment charges

- Prepayment charges

- GST

These charges increase the total cost of borrowing.

Mistakes to Avoid

1. Ignoring APR

APR includes all costs, not just personal loan interest rates

2. Not Comparing Lenders

You may miss better deals

3. Choosing Long Tenure

Increases total interest

4. Borrowing Excess Amount

Leads to unnecessary interest burden

Personal Loan Interest Rates Comparison Table

| Lender Type | Interest Rate (p.a.) | Processing Fee | Approval Speed | Best For |

|---|---|---|---|---|

| Public Sector Banks | 10% – 14% | Low (0.5% – 1%) | Moderate | Low interest seekers |

| Private Banks | 9.99% – 18% | Medium (1% – 2.5%) | Fast | Salaried professionals |

| NBFCs | 13% – 24% | High (1% – 3%) | Very Fast | Low credit score users |

| Fintech Lenders | 18% – 28% | High (2% – 4%) | Instant | Urgent loan needs |

Top Banks Personal Loan Interest Rates Table

| Bank Name | Interest Rate (p.a.) | Loan Amount | Tenure |

|---|---|---|---|

| SBI | 10% – 15% | Up to ₹20 Lakhs | Up to 6 years |

| HDFC Bank | 9.99% – 24% | Up to ₹40 Lakhs | Up to 5 years |

| ICICI Bank | 9.99% – 16.5% | Up to ₹50 Lakhs | Up to 6 years |

| Axis Bank | 9.5% – 22% | Up to ₹40 Lakhs | Up to 5 years |

| Bank of Baroda | 10% onwards | Up to ₹20 Lakhs | Up to 5 years |

Impact of Personal Loan Interest Rates on EMI

| Loan Amount | Interest Rate | Tenure | Approx EMI | Total Payment |

|---|---|---|---|---|

| ₹5,00,000 | 10% | 3 Years | Lower EMI | Lower Cost |

| ₹5,00,000 | 15% | 3 Years | Medium EMI | Medium Cost |

| ₹5,00,000 | 20% | 3 Years | High EMI | Very High Cost |

Quick Insight

- Lower rates = Lower EMI + More savings

- Higher rates = Higher EMI + More financial burden

- Always compare before choosing

Best Time to Take a Personal Loan

- When interest rates are low

- When you have a high credit score

- During festive offers

Advantages of Low Personal Loan Interest Rates

When applying for a loan, one of the most important factors to consider is the personal loan interest rates. A lower rate can make a huge difference in how much you pay over time. Even a small reduction in personal loan interest rates can lead to significant financial benefits.

Let’s explore the major advantages in full detail:

1. Lower EMI (Equated Monthly Installment)

One of the biggest advantages of low personal loan interest rates is that it directly reduces your EMI.

How it works:

The EMI you pay every month includes:

- Principal amount

- Interest amount

When personal loan interest rates are lower, the interest portion in your EMI decreases, which results in a smaller monthly payment.

Why this matters:

- Easier to manage monthly budget

- Less pressure on your salary or income

- More disposable income for other needs

Example:

If you take a ₹5,00,000 loan:

- At 10% interest → Lower EMI

- At 18% interest → Much higher EMI

👉 This clearly shows how lower personal loan interest rates make your monthly payments more affordable.

2. Less Financial Burden

Lower personal loan interest rates significantly reduce your overall financial stress.

What happens with high interest rates:

- You pay more interest over time

- Larger portion of your income goes toward repayment

- Increased risk of missing EMIs

Benefits of low interest rates:

- Reduced total repayment amount

- Better financial stability

- Lower risk of debt trap

When personal loan interest rates are low, you don’t feel overwhelmed by repayments, which improves your financial well-being.

3. Faster Repayment of Loan

Low personal loan interest rates help you repay your loan faster.

How?

- More of your EMI goes toward the principal instead of interest

- Outstanding loan amount reduces quickly

Advantages:

- Become debt-free sooner

- Improve your credit score

- Increase eligibility for future loans

When personal loan interest rates are high, a large portion of EMI goes toward interest, slowing down repayment. But with low rates, you clear your loan much faster.

4. Better Savings and Financial Growth

Another major benefit of low personal loan interest rates is that it allows you to save more money.

Why savings improve:

- Lower EMI = more money left each month

- Lower total interest = less money wasted

Where you can use the savings:

- Emergency fund

- Investments (mutual funds, stocks, FD)

- Daily expenses or lifestyle improvements

Over time, saving on personal loan interest rates can help you build wealth instead of losing money on high interest payments.

5. Improved Financial Planning

Low personal loan interest rates make it easier to plan your finances.

Benefits:

- Predictable EMIs

- Better budgeting

- More control over expenses

With lower rates, you can allocate money efficiently toward savings, investments, and other goals.

6. Reduced Total Cost of Borrowing

The total amount you repay depends heavily on personal loan interest rates.

Example:

Loan: ₹5,00,000 for 3 years

- At 10% → Much lower total repayment

- At 18% → Significantly higher repayment

👉 Lower personal loan interest rates reduce the total cost of the loan, saving you thousands of rupees.

7. Lower Risk of Default

When EMIs are affordable due to low personal loan interest rates, you are less likely to miss payments.

Benefits:

- Maintains good credit score

- Avoids penalties

- Keeps your financial profile strong

8. Flexibility in Loan Tenure

Low personal loan interest rates give you more flexibility:

- You can choose shorter tenure without increasing EMI too much

- Or choose longer tenure with very comfortable EMIs

Disadvantages of High Personal Loan Interest Rates

While personal loans are easy to access, high personal loan interest rates can create serious financial problems if not managed properly. Many borrowers focus only on loan approval and ignore the long-term impact of high personal loan interest rates, which can lead to heavy financial pressure.

Let’s understand the major disadvantages in detail:

1. Higher EMIs (Equated Monthly Installments)

One of the most immediate effects of high personal loan interest rates is an increase in your EMI.

How it works:

Your EMI consists of:

- Principal repayment

- Interest payment

When personal loan interest rates are high, the interest portion increases, which directly raises your monthly EMI.

Impact on your finances:

- A large portion of your monthly income goes toward loan repayment

- Less money is available for daily expenses

- Difficulty in maintaining a balanced budget

Example:

If you take a ₹5,00,000 loan:

- At 10% → EMI is manageable

- At 20% → EMI becomes significantly higher

👉 This shows how high personal loan interest rates can make your loan expensive from the very beginning.

2. Financial Stress

High personal loan interest rates often lead to continuous financial pressure.

Why this happens:

- Higher EMIs strain your monthly income

- Unexpected expenses become harder to manage

- Savings may get reduced or completely exhausted

Long-term effects:

- Anxiety about meeting monthly payments

- Reduced quality of life

- Difficulty handling emergencies

When personal loan interest rates are high, borrowers may feel trapped in a cycle of repayment, which affects both financial and mental well-being.

3. Increased Debt Burden

Another major disadvantage of high personal loan interest rates is the increase in total debt.

What happens:

- You end up paying much more than the borrowed amount

- A large part of your payment goes toward interest, not principal

Example:

Loan Amount: ₹5,00,000

- At low interest → You pay slightly more than ₹5,00,000

- At high interest → You may repay ₹7,00,000 or more

👉 This clearly shows how high personal loan interest rates increase your total repayment am

4. Slower Loan Repayment

With high personal loan interest rates, repayment becomes slower.

Why?

- A larger portion of EMI goes toward interest

- Principal reduces very slowly

Impact:

- You remain in debt for a longer time

- It delays your financial freedom

5. Reduced Savings and Investments

High personal loan interest rates leave you with less money for savings.

Consequences:

- Difficulty building an emergency fund

- Reduced investment in assets like mutual funds or stocks

- Missed opportunities for wealth creation

6. Higher Risk of Default

When EMIs are too high due to high personal loan interest rates, the risk of missing payments increases.

Effects of default:

- Late payment penalties

- Damage to credit score

- Difficulty getting future loans

7. Limited Financial Flexibility

High personal loan interest rates reduce your financial flexibility.

Why:

- Most of your income is locked into EMIs

- Less freedom to spend or invest

- Hard to take additional loans if needed

Tips to Compare Personal Loan Interest Rates

- Check minimum and maximum rates

- Compare APR

- Look at hidden charges

- Use EMI calculators

Digital Tools to Check Interest Rates

- Bank websites

- Loan comparison platforms

- EMI calculators

Who Should Check Personal Loan Interest Rates?

- Salaried employees

- Self-employed individuals

- Students

- Business owners

Real-Life Example

Let’s understand impact of personal loan interest rates:

Loan Amount: ₹5,00,000

Tenure: 3 years

| Interest Rate | EMI | Total Payment |

|---|---|---|

| 10% | Lower EMI | Lower cost |

| 18% | Higher EMI | Much higher cost |

👉 This shows why choosing the right personal loan interest rates is crucial.

Future Trends in Personal Loan Interest Rates

- Digital lending increasing

- AI-based risk assessment

- Faster approvals

- Competitive rates

10 FAQs on Personal Loan Interest Rates

1. What are personal loan interest rates?

Personal loan interest rates are the charges applied by banks or financial institutions on the amount you borrow. These rates are usually expressed as a percentage per year (per annum). The interest is added to your loan amount and repaid through EMIs over the loan tenure. Higher personal loan interest rates mean higher overall repayment.

2. What is the current personal loan interest rate in India?

In India, personal loan interest rates typically range from 10% to 24% per annum, depending on the lender, your credit score, income, and employment type. Some banks may offer lower personal loan interest rates to customers with excellent credit profiles.

3. What factors affect personal loan interest rates?

Several factors influence personal loan interest rates, including:

- Credit score (CIBIL score)

- Monthly income

- Employment type (salaried or self-employed)

- Loan amount and tenure

- Existing debts

A better financial profile usually results in lower personal loan interest rates.

4. How can I get the lowest personal loan interest rates?

To get the lowest personal loan interest rates, you should:

- Maintain a high credit score (750+)

- Pay EMIs and bills on time

- Compare multiple lenders

- Choose a shorter loan tenure

- Apply with your existing bank

These steps improve your chances of securing lower personal loan interest rates.

5. Are personal loan interest rates fixed or variable?

Personal loan interest rates can be either:

- Fixed: Remain constant throughout the loan tenure

- Floating: Change based on market conditions

Most personal loans in India come with fixed personal loan interest rates, making EMIs predictable.

6. How do personal loan interest rates affect EMI?

Personal loan interest rates directly impact your EMI.

- Higher rates → Higher EMI

- Lower rates → Lower EMI

Even a small difference in personal loan interest rates can significantly change your monthly payment and total repayment.

7. Can I negotiate personal loan interest rates?

Yes, you can negotiate personal loan interest rates, especially if:

- You have a high credit score

- You have a stable income

- You are an existing customer of the bank

Many lenders offer better personal loan interest rates to low-risk borrowers.

8. Why are personal loan interest rates higher than other loans?

Personal loan interest rates are higher because personal loans are unsecured loans, meaning no collateral is required. Since the lender takes more risk, they charge higher personal loan interest rates compared to secured loans like home loans or car loans.

9. Does loan tenure affect personal loan interest rates?

Loan tenure does not always change the personal loan interest rates, but it affects the total interest paid.

- Longer tenure → More total interest

- Shorter tenure → Less total interest but higher EMI

Choosing the right tenure helps manage your loan efficiently.

10. Is a lower personal loan interest rate always better?

Yes, lower personal loan interest rates are generally better because:

- They reduce EMI

- Lower total repayment

- Decrease financial burden

However, you should also check other charges like processing fees and penalties along with personal loan interest rates.

Final Thoughts and Conclusion

Choosing the right loan is not just about getting quick approval or a high loan amount—it’s about understanding the long-term impact of personal loan interest rates on your financial life. Many borrowers underestimate how much these rates influence their total repayment, monthly budget, and overall financial stability.

Throughout this guide, we’ve seen that personal loan interest rates play a central role in determining how affordable or expensive your loan will be. A lower rate can make your EMIs manageable, reduce your financial burden, and help you repay the loan faster. On the other hand, higher personal loan interest rates can significantly increase your EMI, stretch your finances, and keep you in debt for a longer period.

One of the most important takeaways is that even a small difference in personal loan interest rates—just 1% or 2%—can lead to substantial savings over time. That’s why it is always recommended to compare multiple lenders, check your eligibility, and negotiate whenever possible before finalizing your loan.

Another key point to remember is that personal loan interest rates are not random. They are based on your financial profile, including your credit score, income, job stability, and repayment history. By maintaining a strong credit profile and managing your finances responsibly, you can qualify for better rates and save a significant amount of money.

It’s also important to look beyond just the interest rate. While personal loan interest rates are crucial, you should also consider additional charges like processing fees, prepayment penalties, and late payment fees. A loan with slightly higher interest but lower overall charges may sometimes be a better deal.

In today’s digital era, comparing personal loan interest rates has become easier than ever. With online tools, EMI calculators, and comparison platforms, you can evaluate multiple options and make informed decisions within minutes. Taking the time to research and understand your options can prevent financial stress in the future.

Final Advice

- Always aim for the lowest possible personal loan interest rates

- Maintain a good credit score to improve your eligibility

- Choose a loan tenure that balances EMI affordability and total interest

- Avoid borrowing more than you actually need

- Read all terms and conditions carefully before signing

Conclusion

In simple terms, personal loan interest rates are the backbone of your borrowing decision. They determine how much you pay, how long you stay in debt, and how comfortable your financial journey will be.

A smart borrower doesn’t just take a loan—they choose it wisely. By understanding and carefully evaluating personal loan interest rates, you can reduce costs, avoid unnecessary stress, and achieve your financial goals with confidence.

👉 Remember:

The lower the interest rate, the lighter your financial future will be.