Becoming debt-free is one of the most powerful financial goals anyone can achieve. Among the most popular repayment strategies, the debt snowball vs debt avalanche methods stand out as the most effective and widely used approaches. Both strategies help you eliminate debt systematically, reduce stress, and build financial discipline, but they work in very different ways.

In this detailed guide, we will explore everything you need to know about debt snowball vs debt avalanche, how each method works, their pros and cons, real-life examples, and how to choose the best strategy for your financial situation. Whether you’re struggling with credit card debt, personal loans, or multiple EMIs, this guide will help you take control of your finances.

Introduction to Debt Repayment Strategies

When it comes to paying off debt, most people feel overwhelmed by multiple balances, interest rates, and due dates. That’s where structured repayment methods come in.

The concept of debt snowball vs debt avalanche is designed to simplify debt repayment by giving you a clear step-by-step system. Instead of randomly paying debts, you follow a structured method that maximizes either psychological motivation or financial savings.

The debt snowball vs debt avalanche debate often comes down to behavior vs mathematics. One focuses on quick emotional wins, while the other focuses on saving the most money on interest.

Understanding the debt snowball vs debt avalanche approach can help you stay consistent and finally break free from debt cycles.

Many financial experts recommend choosing one of these methods because the debt snowball vs debt avalanche system provides clarity and discipline, which are essential for long-term financial success.

1. Understanding Debt Repayment Methods

The idea behind debt snowball vs debt avalanche is simple: instead of paying all debts equally, you prioritize them in a specific order.

In the debt snowball vs debt avalanche system, you list all your debts, then decide which one to attack first based on either balance size or interest rate.

The debt snowball vs debt avalanche approach helps you stay organized and focused. Without a system, many people lose track and end up paying more interest over time.

By using debt snowball vs debt avalanche, you create momentum and structure in your repayment journey, making it easier to stay committed for the long term.

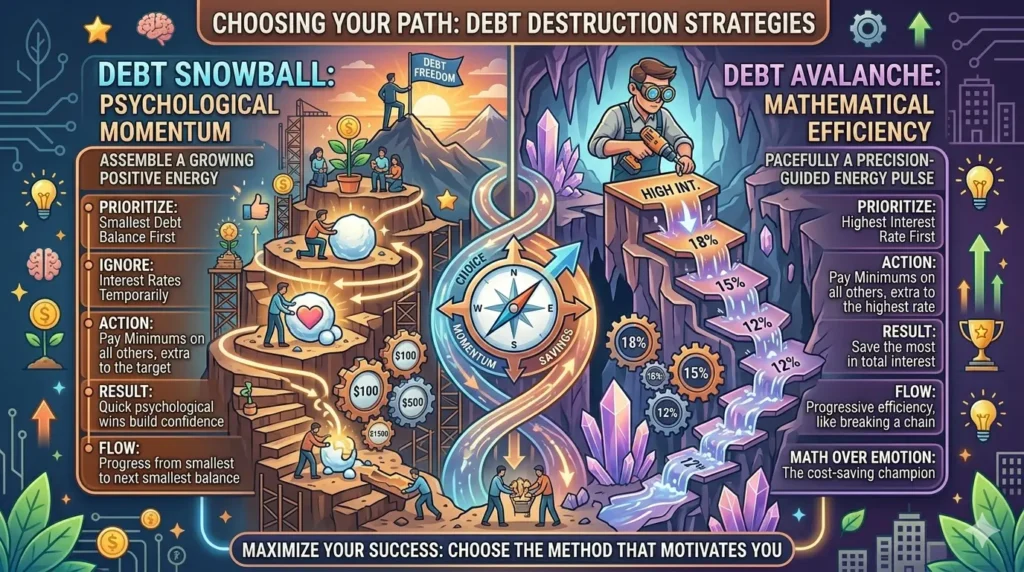

2. Debt Snowball Method Explained

The debt snowball vs debt avalanche discussion often starts with the debt snowball method because it is the most psychologically motivating approach.

In the debt snowball method (part of debt snowball vs debt avalanche), you arrange your debts from smallest balance to largest balance. You pay minimum payments on all debts except the smallest one. You aggressively pay off the smallest debt first.

Once the smallest debt is cleared, you move to the next smallest, creating a “snowball effect.”

The debt snowball vs debt avalanche comparison shows that the snowball method focuses on quick wins. These early victories build motivation and keep you consistent.

How Debt Snowball Works:

- List debts from smallest to largest.

- Pay minimum on all debts.

- Put extra money toward smallest debt.

- Once paid off, move to next smallest.

In the debt snowball vs debt avalanche debate, the snowball method is ideal for people who need motivation and emotional reinforcement.

3. Debt Avalanche Method Explained

The debt snowball vs debt avalanche comparison would be incomplete without understanding the avalanche method.

In the debt avalanche method (a key part of debt snowball vs debt avalanche), you prioritize debts based on interest rates. You pay off the debt with the highest interest rate first while making minimum payments on others.

This method saves more money in the long run because high-interest debts grow faster.

How Debt Avalanche Works:

- List debts from highest to lowest interest rate.

- Pay minimum on all debts.

- Focus extra payments on highest interest debt.

- Move down the list as each debt is cleared.

In the debt snowball vs debt avalanche comparison, the avalanche method is mathematically efficient and reduces total interest paid.

However, the debt snowball vs debt avalanche analysis shows that it may take longer to see early progress, which can affect motivation.

4. Key Differences: Debt Snowball vs Debt Avalanche

The debt snowball vs debt avalanche methods differ in structure, psychology, and financial outcome.

1. Focus Area

- Snowball focuses on smallest balance first

- Avalanche focuses on highest interest rate first

2. Motivation vs Savings

- debt snowball vs debt avalanche shows snowball is motivation-driven

- Avalanche is savings-driven

3. Speed of Results

- Snowball gives faster small wins

- Avalanche may take longer initially but saves more money

4. Total Interest Paid

- Snowball may result in higher interest

- Avalanche minimizes interest cost

5. Psychological Impact

- Snowball builds confidence quickly

- Avalanche requires discipline and patience

Overall, the debt snowball vs debt avalanche comparison highlights that both strategies work, but for different personality types.

5. Which Is Better: Debt Snowball vs Debt Avalanche?

When comparing debt snowball vs debt avalanche, there is no universal “best” method that works for everyone. The right choice depends heavily on your personality, financial habits, emotional triggers, income stability, and ability to stay consistent over time. Both strategies are proven to work, but they succeed for different types of people in different situations.

Understanding this section of debt snowball vs debt avalanche is very important because many people fail in debt repayment not because they chose the wrong strategy, but because they chose a strategy they could not stick with long enough.

1. Motivation vs Mathematics in Debt Snowball vs Debt Avalanche

The core difference in debt snowball vs debt avalanche comes down to two powerful forces in personal finance:

- Human behavior (motivation, emotions, discipline)

- Mathematical efficiency (interest savings, cost reduction)

The debt snowball method is designed for behavior. It prioritizes emotional wins. On the other hand, the debt avalanche method is designed for mathematics. It prioritizes financial optimization.

In debt snowball vs debt avalanche, this difference is crucial because:

- If motivation is your biggest challenge, snowball wins

- If discipline is your strongest skill, avalanche wins

Many people assume that saving more money automatically makes a method better, but in debt snowball vs debt avalanche, consistency matters more than theory.

2. When Debt Snowball Is the Better Choice

In the debt snowball vs debt avalanche comparison, the snowball method is often better for individuals who struggle with staying consistent or feel overwhelmed by debt.

You should choose the snowball method if:

You feel emotionally stressed about debt

If your debts make you anxious or mentally exhausted, the snowball method helps reduce stress quickly. Small victories give a sense of control, which is very important in early stages of repayment.

You need visible progress to stay motivated

In debt snowball vs debt avalanche, snowball is powerful because you eliminate smaller debts quickly. Each cleared account gives psychological relief and motivation to continue.

You have multiple small debts

If your financial profile includes many small credit cards, personal loans, or BNPL (buy now pay later) accounts, snowball helps you clean up your financial life faster.

You have struggled with consistency in the past

If you often start repayment plans but quit midway, the snowball method helps break that pattern through constant reinforcement.

In short, in debt snowball vs debt avalanche, snowball is ideal for building momentum and developing financial discipline step by step.

3. When Debt Avalanche Is the Better Choice

In the debt snowball vs debt avalanche debate, the avalanche method is financially superior in terms of total savings, but it requires patience and strong discipline.

You should choose the avalanche method if:

You are financially disciplined

If you can stick to a long-term plan without needing emotional rewards, avalanche is very effective.

You want to save the most money possible

One of the biggest advantages in debt snowball vs debt avalanche is that avalanche minimizes total interest paid. High-interest debts like credit cards are eliminated first, reducing long-term financial burden.

You understand long-term planning

If you are focused on wealth building, investing, or long-term financial independence, avalanche aligns better with those goals.

Your debts have high interest variation

If one or two debts have significantly higher interest rates than others, avalanche becomes mathematically more efficient.

In debt snowball vs debt avalanche, avalanche rewards patience with financial savings, but it does not provide quick emotional wins.

4. Psychological Factor in Debt Snowball vs Debt Avalanche

One of the most overlooked aspects of debt snowball vs debt avalanche is psychology.

Money management is not just about numbers—it is about behavior patterns. Studies in behavioral finance show that people are more likely to stick to plans when they see immediate results.

This is why the snowball method often feels easier at the beginning of the debt snowball vs debt avalanche journey. It builds confidence and creates a sense of achievement.

However, the avalanche method requires delayed gratification. In debt snowball vs debt avalanche, this can feel slower at first, even though it is more efficient in the long run.

5. Consistency Is More Important Than Method in Debt Snowball vs Debt Avalanche

A major truth in debt snowball vs debt avalanche is that consistency beats strategy.

It doesn’t matter which method you choose if you stop halfway. Both methods fail if:

- You miss payments regularly

- You take on new unnecessary debt

- You don’t follow your repayment plan

- You lose motivation early

In debt snowball vs debt avalanche, the biggest success factor is not the method—it is your ability to stay committed for months or years until debt is completely eliminated.

6. Hybrid Approach in Debt Snowball vs Debt Avalanche

Interestingly, many financial experts recommend a hybrid approach in debt snowball vs debt avalanche.

This means combining both strategies:

- Start with snowball to build motivation

- Switch to avalanche for long-term savings

In debt snowball vs debt avalanche, this hybrid model helps balance emotional motivation with financial efficiency.

For example:

- Pay off 1–2 smallest debts first (snowball)

- Then switch to highest interest debt (avalanche)

This approach works well for people who need both psychological wins and financial optimization.

7. Real-Life Example of Debt Snowball vs Debt Avalanche

Let’s understand debt snowball vs debt avalanche with a simple example:

Imagine you have three debts:

- Credit Card A: $500 (18% interest)

- Personal Loan B: $2,000 (10% interest)

- Credit Card C: $5,000 (25% interest)

Snowball Method:

You pay off $500 first because it is the smallest.

Avalanche Method:

You pay off $5,000 first because it has the highest interest rate.

In debt snowball vs debt avalanche, both methods will eventually clear all debts—but:

- Snowball gives faster emotional satisfaction

- Avalanche saves more money on interest

8. Final Decision Framework in Debt Snowball vs Debt Avalanche

To decide properly in debt snowball vs debt avalanche, ask yourself:

- Do I need motivation or savings?

- Do I quit financial plans easily?

- Am I more emotional or analytical with money?

- Can I wait for long-term results?

If you answer honestly, your choice in debt snowball vs debt avalanche becomes clear6. Step-by-Step Guide to Debt Snowball Method

To apply the debt snowball vs debt avalanche strategy using snowball, follow these steps:

Step 1: List All Debts

Write down all debts including credit cards, loans, and EMIs.

Step 2: Arrange by Balance

Sort from smallest to largest.

Step 3: Set Minimum Payments

Pay minimum on all debts except the smallest.

Step 4: Attack Smallest Debt

Put extra income toward the smallest debt.

Step 5: Roll Payments Forward

Once a debt is cleared, move to the next.

The debt snowball vs debt avalanche method shows snowball works best for emotional momentum.

7. Step-by-Step Guide to Debt Avalanche Method

Now let’s apply the debt snowball vs debt avalanche approach using avalanche:

Step 1: List All Debts

Include interest rates for each debt.

Step 2: Sort by Interest Rate

Highest interest first.

Step 3: Pay Minimums

Keep all accounts active.

Step 4: Focus on High Interest Debt

Put extra payments toward highest interest debt.

Step 5: Repeat Process

Move down the list after each payoff.

The debt snowball vs debt avalanche method shows avalanche is best for minimizing financial cost.

8. Common Mistakes in Debt Snowball vs Debt Avalanche

Many people fail when using debt snowball vs debt avalanche due to common mistakes:

- Not sticking to one method

- Ignoring budgeting

- Taking new debt while repaying old debt

- Losing motivation early

- Not tracking progress

The debt snowball vs debt avalanche system only works when consistency is maintained.

10 FAQs on Debt Snowball vs Debt Avalanche

Below are the most commonly asked questions about debt snowball vs debt avalanche, explained in a simple, detailed, and practical way to help you choose the right debt repayment strategy and stay on track toward financial freedom.

1. What is the main difference between debt snowball vs debt avalanche?

The main difference in debt snowball vs debt avalanche is the order in which you pay off your debts.

- In the debt snowball method, you pay off the smallest debt first, regardless of interest rate.

- In the debt avalanche method, you pay off the debt with the highest interest rate first, regardless of balance.

In debt snowball vs debt avalanche, snowball focuses on motivation and quick wins, while avalanche focuses on saving the most money on interest.

Both strategies are effective in debt snowball vs debt avalanche, but they serve different psychological and financial goals.

2. Which method saves more money: debt snowball vs debt avalanche?

In debt snowball vs debt avalanche, the debt avalanche method usually saves more money.

This is because you pay off high-interest debts first, which reduces the total interest that accumulates over time. Credit cards and payday loans often have very high interest rates, so eliminating them early reduces long-term costs.

The snowball method in debt snowball vs debt avalanche may cost slightly more in interest, but it can help people stay motivated and consistent.

3. Which method is faster: debt snowball vs debt avalanche?

Speed in debt snowball vs debt avalanche depends on how you define “faster.”

- The debt snowball method feels faster because you eliminate small debts quickly, giving emotional wins.

- The debt avalanche method may be mathematically faster in reducing total repayment time, but progress may feel slower at the beginning.

So in debt snowball vs debt avalanche, snowball feels faster emotionally, while avalanche is faster financially.

4. Is debt snowball vs debt avalanche suitable for beginners?

Yes, both methods in debt snowball vs debt avalanche are suitable for beginners.

However, beginners often prefer the debt snowball method because it is easier to understand and provides quick motivation.

In debt snowball vs debt avalanche, snowball helps beginners stay consistent because they see progress quickly, which reduces the chance of giving up early.

Avalanche is also beginner-friendly but requires more discipline and patience.

5. Can I switch between debt snowball vs debt avalanche methods?

Yes, you can switch between debt snowball vs debt avalanche methods anytime.

Many people start with the snowball method to gain motivation and later switch to avalanche to save more money.

In debt snowball vs debt avalanche, this hybrid approach is common and highly effective because it balances emotional motivation with financial efficiency.

The key is consistency, not the method itself.

6. Which method is better for credit card debt: debt snowball vs debt avalanche?

For credit card debt, the debt snowball vs debt avalanche comparison clearly favors the avalanche method.

Credit cards usually have high interest rates, so paying them off first saves a significant amount of money.

However, in debt snowball vs debt avalanche, if you have multiple credit cards and feel overwhelmed, starting with the smallest balance (snowball) may help you stay motivated.

So the best choice depends on your emotional discipline and financial situation.

7. What happens if I take new debt while using debt snowball vs debt avalanche?

Taking new debt while using debt snowball vs debt avalanche can seriously delay your progress.

Both methods require discipline to avoid additional borrowing. If you keep adding new debt, you will never fully benefit from either strategy.

In debt snowball vs debt avalanche, success depends not only on repayment strategy but also on stopping new debt accumulation.

Without this discipline, both methods lose effectiveness.

8. How long does it take to become debt-free using debt snowball vs debt avalanche?

The time required in debt snowball vs debt avalanche depends on:

- Total debt amount

- Monthly repayment capacity

- Interest rates

- Consistency

In general:

- The debt snowball method may take slightly longer financially but helps people stay consistent.

- The debt avalanche method may reduce total repayment time and interest cost.

In debt snowball vs debt avalanche, the biggest factor is how much extra money you can pay each month.

9. Can debt snowball vs debt avalanche affect my credit score?

Yes, both methods in debt snowball vs debt avalanche can positively impact your credit score over time.

As you pay down debt:

- Credit utilization decreases

- Payment history improves

- Overall financial responsibility increases

However, in debt snowball vs debt avalanche, the method you choose does not directly impact your credit score. What matters is making on-time payments consistently.

10. Which is ultimately better: debt snowball vs debt avalanche?

There is no absolute winner in debt snowball vs debt avalanche.

- Choose debt snowball if you need motivation, emotional wins, and structure.

- Choose debt avalanche if you want to minimize interest and are disciplined.

In debt snowball vs debt avalanche, the best method is the one you can stick with until you become completely debt-free.

The ultimate goal of debt snowball vs debt avalanche is not just paying off debt—it is building long-term financial discipline and achieving financial freedom.

Final Thought and Conclusion: Debt Snowball vs Debt Avalanche

When it comes to debt snowball vs debt avalanche, the most important takeaway is that both methods are powerful, proven, and effective ways to become debt-free. There is no single “perfect” strategy that works for everyone—success depends more on your behavior, discipline, and consistency than the method itself.

The debt snowball vs debt avalanche approach teaches an important life lesson: personal finance is not just about numbers, it is also about psychology. Money decisions are deeply influenced by motivation, habits, and emotional resilience.

If you choose the debt snowball method, you gain momentum through quick wins. You start small, eliminate debts one by one, and build confidence as you see progress. This method is especially helpful for people who feel overwhelmed or struggle with staying consistent. In debt snowball vs debt avalanche, snowball is the motivation-driven path that keeps you emotionally engaged.

On the other hand, the debt avalanche method is the most financially efficient strategy. It reduces the total interest you pay over time and helps you become debt-free in the most cost-effective way possible. In debt snowball vs debt avalanche, avalanche is the logic-driven path designed for long-term savings and financial optimization.

However, the real secret in debt snowball vs debt avalanche is not choosing the “best” method—it is choosing the method you will actually follow until the end. Many people fail in debt repayment not because they picked the wrong strategy, but because they gave up midway.

That is why consistency matters more than strategy in debt snowball vs debt avalanche. Whether you prefer emotional motivation or mathematical efficiency, the goal remains the same: eliminating debt completely and building a stable financial future.

In conclusion, the debt snowball vs debt avalanche debate does not have a universal winner. The best method is the one that fits your mindset, keeps you consistent, and helps you stay committed for the long term. If you stay disciplined and focused, both paths will eventually lead you to the same destination—financial freedom, peace of mind, and a debt-free life.