Roth IRA vs 401k difference is one of the most important steps in building long-term financial security in the United States. Whether you are just starting your career or planning for retirement, choosing between these two powerful retirement accounts can significantly impact your future wealth, tax savings, and financial freedom.

In this detailed guide, we will break down everything you need to know about the Roth IRA vs 401k difference, including tax treatment, contribution limits, withdrawal rules, employer benefits, investment flexibility, and which option may be best for you.

By the end of this article, you will have a crystal-clear understanding of the Roth IRA vs 401k difference and how to use both accounts strategically for maximum retirement growth.

What is a Roth IRA?

A Roth IRA (Individual Retirement Account) is a retirement savings account that allows you to invest after-tax income. The biggest benefit is that your money grows tax-free, and qualified withdrawals in retirement are completely tax-free.

One major part of the Roth IRA vs 401k difference is how taxes are handled. With a Roth IRA, you pay taxes now instead of later.

Key Features of Roth IRA:

- Contributions are made with after-tax dollars

- Tax-free growth

- Tax-free withdrawals in retirement (if rules are followed)

- No required minimum distributions (RMDs)

When analyzing the Roth IRA vs 401k difference, Roth IRAs are often considered more flexible and tax-efficient for long-term investors.

Another important aspect of the Roth IRA vs 401k difference is income eligibility, which we will discuss later.

What is a 401(k)?

A 401(k) is an employer-sponsored retirement plan that allows employees to save and invest pre-tax income. This means your taxable income is reduced today, but you pay taxes when you withdraw in retirement.

Understanding the Roth IRA vs 401k difference requires knowing that a 401(k) often includes employer contributions or “matching,” which is a major advantage.

Key Features of 401(k):

- Pre-tax contributions (Traditional 401k)

- Employer matching contributions

- Tax-deferred growth

- Required minimum distributions (RMDs) after age 73

A major part of the Roth IRA vs 401k difference is that 401(k)s are tied to your employer, while Roth IRAs are individually controlled.

The Roth IRA vs 401k difference becomes clearer when comparing flexibility and employer involvement.

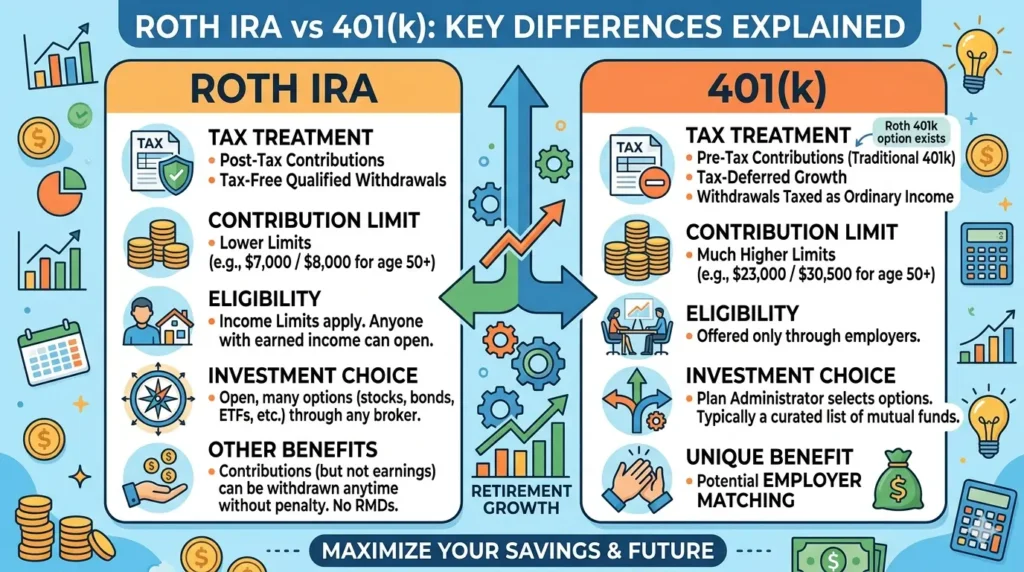

Roth IRA vs 401(k) Difference Overview

At a high level, the Roth IRA vs 401k difference is best understood by breaking it into five major areas: tax timing, employer involvement, contribution limits, withdrawal rules, and investment choices. Each of these factors plays a key role in deciding which account fits your financial goals and retirement strategy.

Below is a detailed breakdown of each point to help you clearly understand the Roth IRA vs 401k difference in real-life terms.

1. Tax Timing (Now vs Later)

One of the most important aspects of the Roth IRA vs 401k difference is how and when you pay taxes.

Roth IRA (Pay Taxes Now)

With a Roth IRA, you contribute money that has already been taxed. This means:

- You do not get a tax deduction today

- Your money grows completely tax-free

- You can withdraw it tax-free in retirement (if rules are met)

This structure makes Roth IRAs attractive for people who believe taxes will be higher in the future. In the Roth IRA vs 401k difference, this is called “tax-free future income.”

401(k) (Pay Taxes Later)

With a traditional 401(k), contributions are made before taxes are deducted. This means:

- You reduce your taxable income today

- You pay taxes when you withdraw in retirement

- Your investments grow tax-deferred until withdrawal

In the Roth IRA vs 401k difference, this is called “tax-deferred growth.”

Why This Matters

The timing of taxes affects your long-term wealth. If you choose wrong, you may end up paying higher taxes later. That’s why tax timing is the most critical part of the Roth IRA vs 401k difference.

2. Employer Involvement

Another major factor in the Roth IRA vs 401k difference is whether your employer is involved.

Roth IRA (No Employer Involvement)

A Roth IRA is completely independent:

- You open it yourself at a bank or brokerage

- No employer contributions

- You have full control over the account

This independence is a key part of the Roth IRA vs 401k difference, making it ideal for personal financial control.

401(k) (Employer-Sponsored Plan)

A 401(k) is offered through your employer:

- Contributions are often automated from your paycheck

- Many employers offer matching contributions

- Account options are limited by employer selection

The employer match is one of the biggest advantages in the Roth IRA vs 401k difference, because it is essentially free money added to your retirement savings.

Why This Matters

Employer involvement can significantly boost your retirement savings. If you ignore this part of the Roth IRA vs 401k difference, you may lose valuable matching contributions.

3. Contribution Limits

The Roth IRA vs 401k difference becomes very clear when comparing how much money you can invest each year.

Roth IRA Contribution Limits

- Lower annual contribution limit

- Income restrictions apply

- Ideal for moderate savers or additional retirement savings

Because of these limits, the Roth IRA is often used as a supplemental account in the Roth IRA vs 401k difference strategy.

401(k) Contribution Limits

- Much higher contribution limits

- Allows large-scale retirement savings

- Often includes employer contributions on top of your own

This is a major advantage in the Roth IRA vs 401k difference, especially for high earners who want to maximize tax-advantaged savings.

Why This Matters

If your goal is aggressive retirement saving, the Roth IRA vs 401k difference clearly favors 401(k) due to higher contribution capacity.

4. Withdrawal Rules

Withdrawal flexibility is another key part of the Roth IRA vs 401k difference.

Roth IRA Withdrawal Rules

- Contributions can usually be withdrawn anytime without penalty

- Earnings are tax-free if conditions are met (age 59½ and 5-year rule)

- More flexibility for emergencies

This makes Roth IRAs highly flexible in the Roth IRA vs 401k difference, especially for younger investors.

401(k) Withdrawal Rules

- Withdrawals before retirement age usually have penalties

- Taxes must be paid on withdrawals

- Limited flexibility for early access

This makes 401(k)s more restrictive in the Roth IRA vs 401k difference.

Why This Matters

If you want access to your money in emergencies, the Roth IRA vs 401k difference strongly favors Roth IRA due to its flexibility.

5. Investment Choices

Investment flexibility is another important factor in the Roth IRA vs 401k difference.

Roth IRA Investment Options

- Wide range of investment choices

- Stocks, ETFs, bonds, mutual funds, REITs, and more

- Full control over your portfolio

This makes Roth IRAs highly customizable in the Roth IRA vs 401k difference.

401(k) Investment Options

- Limited selection chosen by employer

- Usually includes a few mutual funds or target-date funds

- Less control compared to Roth IRA

This limitation is a key drawback in the Roth IRA vs 401k difference.

Why This Matters

Investment control can significantly impact long-term returns. More flexibility in the Roth IRA vs 401k difference often leads to better diversification strategies for informed investorsTax Treatment: The Biggest Roth IRA vs 401k Difference

Taxes are the most important factor in the Roth IRA vs 401k difference.

Roth IRA Tax Structure:

- Pay taxes before contribution

- No taxes on qualified withdrawals

401(k) Tax Structure:

- Contributions are tax-deductible

- Taxes paid on withdrawals

The Roth IRA vs 401k difference in taxation determines how your retirement income will be affected later.

If you expect to be in a higher tax bracket in retirement, the Roth IRA vs 401k difference may favor Roth IRA.

If you want tax savings today, the Roth IRA vs 401k difference may favor 401(k).

Understanding this Roth IRA vs 401k difference is essential for long-term planning.

Contribution Limits in Roth IRA vs 401k Difference

Another important Roth IRA vs 401k difference is how much you can contribute.

Roth IRA Limits (2026 approx.):

- Around $7,000 per year (varies by IRS updates)

- Income restrictions apply

401(k) Limits:

- Around $23,000+ per year (employee contribution)

- Higher total with employer match

The Roth IRA vs 401k difference clearly shows that 401(k)s allow much higher savings potential.

High-income earners often notice this Roth IRA vs 401k difference strongly because Roth IRAs have income caps.

The contribution structure is a key Roth IRA vs 401k difference for aggressive savers.

Employer Match and Roth IRA vs 401k Difference

One major advantage in the Roth IRA vs 401k difference is employer matching.

401(k):

- Employers may match 3%–6% of salary

- Free money for retirement

Roth IRA:

- No employer contributions

This makes the Roth IRA vs 401k difference significant for employees who want extra retirement income.

Losing employer match is one of the biggest mistakes in understanding the Roth IRA vs 401k difference.

Withdrawal Rules in Roth IRA vs 401k Difference

Withdrawal rules are another major Roth IRA vs 401k difference.

Roth IRA:

- Contributions can be withdrawn anytime tax-free

- Earnings tax-free after age 59½ (with rules)

401(k):

- Withdrawals taxed as income

- Early withdrawal penalties may apply

The Roth IRA vs 401k difference in flexibility makes Roth IRA more accessible in emergencies.

However, penalties make 401(k) less flexible, highlighting another Roth IRA vs 401k difference.

Required Minimum Distributions (RMDs)

The Roth IRA vs 401k difference becomes very important in retirement age rules.

Roth IRA:

- No RMDs during owner’s lifetime

401(k):

- RMDs required starting around age 73

This Roth IRA vs 401k difference means Roth IRAs are better for estate planning and long-term tax control.

Many retirees prefer Roth IRAs because of this Roth IRA vs 401k difference.

Income Limits in Roth IRA vs 401k Difference

Income eligibility is a key Roth IRA vs 401k difference.

Roth IRA:

- High earners may be restricted

401(k):

- No income limits

This makes the Roth IRA vs 401k difference important for high-income professionals who cannot fully contribute to Roth IRAs.

A backdoor Roth strategy is often used to manage this Roth IRA vs 401k difference.

Investment Options

Another important Roth IRA vs 401k difference is investment flexibility.

Roth IRA:

- Wide range of investments

- Stocks, ETFs, mutual funds, bonds

401(k):

- Limited investment options chosen by employer

The Roth IRA vs 401k difference here shows Roth IRA offers more control.

Many investors prefer Roth IRAs because of this Roth IRA vs 401k difference.

Early Withdrawal Penalties

The Roth IRA vs 401k difference also applies to penalties.

Roth IRA:

- More flexible with contributions

401(k):

- Strict penalties before retirement age

This Roth IRA vs 401k difference makes Roth IRAs more beginner-friendly.

Emergency access is another key Roth IRA vs 401k difference.

Which is Better: Roth IRA vs 401k Difference

There is no single answer to the Roth IRA vs 401k difference question.

Choose 401(k) if:

- You want employer match

- You want higher contribution limits

- You want tax savings now

Choose Roth IRA if:

- You want tax-free retirement income

- You want flexible withdrawals

- You want no RMDs

The best strategy is often combining both, which balances the Roth IRA vs 401k difference effectively.

Understanding your goals is key to solving the Roth IRA vs 401k difference decision.

Smart Strategy Using Both Accounts

One advanced approach to the Roth IRA vs 401k difference is using both accounts together.

- Contribute enough to 401(k) to get employer match

- Invest in Roth IRA for tax-free growth

- Maximize long-term diversification

This hybrid strategy minimizes the Roth IRA vs 401k difference limitations.

Financial planners often recommend this approach for balancing the Roth IRA vs 401k difference.

Common Mistakes in Roth IRA vs 401k Difference

Many people misunderstand the Roth IRA vs 401k difference, leading to mistakes:

- Ignoring employer match

- Not considering taxes

- Choosing only one account

- Overlooking income limits

Avoiding these mistakes improves your understanding of the Roth IRA vs 401k difference.

Tax Planning and Retirement Strategy

Tax planning is central to the Roth IRA vs 401k difference.

If you expect:

- Higher future taxes → Roth IRA may win

- Lower future taxes → 401(k) may win

This planning makes the Roth IRA vs 401k difference a long-term financial decision, not just an account choice.

Long-Term Wealth Building Perspective

The Roth IRA vs 401k difference also impacts long-term wealth creation.

Both accounts offer compound growth, but taxation changes final outcomes.

Understanding compounding is key in evaluating the Roth IRA vs 401k difference.

Over decades, small tax differences become large wealth gaps, highlighting the importance of the Roth IRA vs 401k difference.

10 Frequently Asked Questions About Roth IRA vs 401(k) Difference

Understanding the Roth IRA vs 401k difference can be confusing for beginners. Below are the most commonly asked questions, answered in detail to help you make informed retirement decisions.

1. What is the main difference between a Roth IRA and a 401(k)?

The primary Roth IRA vs 401k difference is tax treatment.

- Roth IRA: Contributions are made with after-tax dollars, meaning you pay taxes upfront. Withdrawals in retirement are tax-free if rules are followed.

- 401(k): Contributions are pre-tax (for a traditional 401(k)), reducing your taxable income today, but withdrawals in retirement are taxed as ordinary income.

This tax timing difference affects how much money you keep in the long term and is the foundation of the Roth IRA vs 401k difference.

2. Can I contribute to both a Roth IRA and a 401(k)?

Yes. Many financial experts recommend using both. This strategy balances the Roth IRA vs 401k difference:

- Use your 401(k) to maximize employer matching and high contribution limits.

- Use your Roth IRA for tax-free growth and withdrawal flexibility.

This combination allows you to take advantage of both tax-free income and employer benefits.

3. Which account is better for beginners?

For beginners, a Roth IRA is often easier to start because:

- It offers more flexibility for early withdrawals (you can withdraw contributions anytime).

- You have full control over investment choices.

- No employer involvement or complicated paperwork.

However, if your employer offers a 401(k) match, it’s smart to contribute at least enough to get the match, as that’s free money.

4. Does a 401(k) have an employer match?

Yes, one of the biggest advantages of a 401(k) is employer matching.

- Employers may match 3%–6% of your salary.

- Some even offer a dollar-for-dollar match up to a certain limit.

This is a key part of the Roth IRA vs 401k difference because Roth IRAs do not have employer contributions.

5. Can I withdraw money from a Roth IRA anytime?

You can withdraw your contributions from a Roth IRA anytime without penalty or taxes.

- Earnings can be withdrawn tax-free after age 59½ and if the account has been open for at least 5 years (known as the 5-year rule).

- Early withdrawal of earnings may incur taxes and penalties.

This makes Roth IRAs more flexible in emergencies, a major factor in the Roth IRA vs 401k difference.

6. What are the contribution limits for Roth IRA and 401(k)?

Contribution limits differ significantly:

- Roth IRA: Around $7,000 per year (for those under 50), with income restrictions.

- 401(k): Around $23,000 per year (employee contribution) in 2026, with higher limits if you include employer match.

This shows a key part of the Roth IRA vs 401k difference—401(k)s allow for much higher annual contributions, which is important for aggressive savers.

7. Are Roth IRA withdrawals taxed?

No, qualified Roth IRA withdrawals are completely tax-free.

- Qualified withdrawals: Account open for at least 5 years and age 59½ or older.

- This tax-free growth is one of the biggest advantages and a central part of the Roth IRA vs 401k difference.

8. Do 401(k)s have early withdrawal penalties?

Yes. With a traditional 401(k):

- Withdrawals before age 59½ typically incur a 10% penalty plus ordinary income tax.

- Some exceptions exist (like hardship withdrawals), but penalties can reduce your savings.

This is a major difference from Roth IRAs and is an important consideration in the Roth IRA vs 401k difference.

9. Is a Roth IRA suitable for high-income earners?

Roth IRA contributions have income limits:

- For high earners above certain thresholds, direct contributions may not be allowed.

- However, a “backdoor Roth IRA” strategy can allow high earners to contribute indirectly.

In contrast, 401(k)s have no income restrictions, highlighting another important Roth IRA vs 401k difference.

10. Which is better for long-term retirement planning: Roth IRA or 401(k)?

There is no single “better” option. The Roth IRA vs 401k difference depends on your goals, tax situation, and career stage.

- Use a 401(k) to take advantage of employer match and higher contribution limits.

- Use a Roth IRA for tax-free growth, flexible withdrawals, and investment control.

Many financial planners recommend a combined approach, which allows you to benefit from both accounts and strategically manage the Roth IRA vs 401k difference.

Final Thoughts and Conclusion on Roth IRA vs 401(k) Difference

Understanding the Roth IRA vs 401k difference is not just about comparing two retirement accounts—it is about building a smart, long-term financial strategy that supports your future lifestyle, tax planning, and wealth creation goals. Both accounts are powerful tools, but they serve different purposes, and the real advantage comes when you understand how to use them together effectively.

At its core, the Roth IRA vs 401k difference comes down to timing, flexibility, and long-term tax strategy. A 401(k) helps you save more aggressively during your working years by offering tax-deferred contributions and employer matching benefits. On the other hand, a Roth IRA gives you tax-free income in retirement and greater control over your money.

Key Takeaway from Roth IRA vs 401k Difference

The most important lesson in the Roth IRA vs 401k difference is that there is no universal “best” option. Instead, the best choice depends on your personal financial situation:

- If you want to reduce taxes today and maximize employer benefits, the 401(k) is extremely valuable.

- If you want tax-free withdrawals and flexibility in retirement, the Roth IRA is a powerful choice.

When you truly understand the Roth IRA vs 401k difference, you realize that both accounts are designed to complement each other, not compete.

Why Using Both Accounts is the Smartest Strategy

One of the most effective approaches in the Roth IRA vs 401k difference debate is not choosing one account, but using both strategically:

- Start with a 401(k) to secure employer matching contributions (this is essentially free money).

- Add a Roth IRA to build tax-free income for the future.

- Increase contributions gradually as your income grows.

This balanced approach reduces risk, increases tax flexibility, and maximizes long-term savings potential. It also helps you take full advantage of the Roth IRA vs 401k difference instead of being limited by one account type.

Long-Term Financial Impact

The Roth IRA vs 401k difference becomes even more important when viewed over decades. Small tax decisions today can lead to huge differences in retirement wealth later. For example:

- Paying taxes later (401(k)) may help you invest more now.

- Paying taxes upfront (Roth IRA) may help you avoid higher taxes in the future.

Over 20–40 years, compound growth can multiply these differences significantly, making it essential to understand the Roth IRA vs 401k difference early in your career.